Retirement Plans Comparative Table Tax-Free IULs vs. 401(k)s

Retirement Plans Comparative Table

| Tax-Free IUL | 401(k) | 403(b) | IRA | |

|---|---|---|---|---|

| Tax-Free IUL | 401(k) | 403(b) | IRA | |

| Tax-Free / Taxable Income | Tax-Free | Heavily Taxed | Heavily Taxed | Heavily Taxed |

| Penalty-Free Withdrawals | Penalty-Free withdrawals any age | 10% early withdrawal penalty under 59 1/2 | 10% early withdrawal penalty under 59 1/2 | 10% early withdrawal penalty under 59 1/2 |

| Stock Market Losses and Yo-Yo Volatility | No You don't lose money when markets go down. | Yes Unless invested in CD, Money Market or Fixed Annuity | Yes Unless invested in CD, Money Market or Fixed Annuity | Yes Unless invested in CD, Money Market or Fixed Annuity |

| Gains Locked In Annually | Yes You don't give back profits previously earned | No Unless invested in CD, Money Market or Fixed Annuity | No Unless invested in CD, Money Market or Fixed Annuity | No Unless invested in CD, Money Market or Fixed Annuity |

| Earn a reasonable rate of return | Yes You don't lose money when markets go down. Never digging out of an investment hole4. | Maybe | Maybe | Maybe |

| RMDs Required Minimum Distributions | No Government does not tell you when to withdraw money. | Yes | Yes | Yes |

| 2014 Contribution Limits | None Great for catchup Cannot make a single payment | $17,500 401(k) elective deferrals $5,500 catchup if you are age 50 or older. annual compensation limit $260,000 | $17,500 403(b) elective deferrals $5,500 catchup if you are age 50 or older. annual compensation limit $260,000 | $5,500 (6,500 if you are age 50 or older) or your taxable compensation for the year. |

| Tax-Free Death Benefit | Yes Could be substantial vs. IRA, 401(k) or 403(b) | No, plan balance is taxable to beneficiaries | No, plan balance is taxable to beneficiaries | No, plan balance is taxable to beneficiaries |

| Premium Financing and leverage | Yes | No | No | No |

| Government Controlls How much you can contribute; when you must take money out. | No | Yes | Yes | Yes |

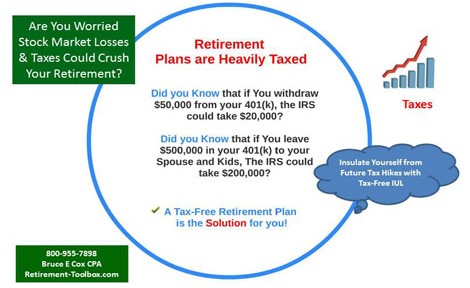

The Retirement Plan Comparative Table illustrates that Tax-Free is Better. The Tax-Free IUL is more flexible. Tax-Free penalty free withdrawals at any age for any reason. Larger contributions are allowed, so it works better at a retirement catch up strategy. It is also safer, as you don’t lose money when the markets go down. Your qualified plans could be subject to substantial market risk.

Watch the Retirement-Toolbox Videos to learn more about the Tax-Free IUL. It is also considered a Tax-Free Pension Alternative and Living Benefits Life Insurance.

The Tax-Free IUL is a life insurance policy with greater focus on living benefits than on death benefits. The Living Benefits make it a great tax-free pension alternative.